The financial landscape is experiencing a seismic shift as the crypto firms’ neobank trend continues to gain unprecedented momentum. Major cryptocurrency companies are now pivoting toward traditional banking services, creating a hybrid model that promises to revolutionize how we manage money. This convergence isn’t just a fad—it’s a strategic evolution that addresses real pain points in both the crypto and traditional banking sectors. As digital assets become mainstream, crypto firms are recognizing that integrating neobank features isn’t optional anymore; it’s essential for survival and growth in an increasingly competitive market.

Crypto Neobank Revolution

What Are Crypto Neobanks?

Crypto neobanks represent a new breed of financial institutions that blend blockchain technology with digital banking services. Unlike traditional banks with physical branches, these platforms operate entirely online, offering cryptocurrency trading, fiat currency accounts, debit cards, and payment processing—all under one digital roof. The neobank trend has exploded globally, with the market projected to reach $2.05 trillion by 2030, and cryptocurrency companies want their share of this lucrative pie.

These innovative platforms eliminate the friction between traditional finance and digital assets. Users no longer need to juggle multiple apps to manage their crypto portfolio and everyday banking needs. This seamless integration is precisely what’s driving crypto firms to invest billions in neobank infrastructure.

The Evolution from Pure Crypto Platforms

The journey from pure cryptocurrency exchanges to full-service neobanks marks a significant maturation of the industry. Early crypto platforms focused exclusively on buying, selling, and trading digital assets. However, as the market evolved, these companies realized that customers needed more than just crypto services—they wanted comprehensive financial solutions.

This realization sparked the crypto firms’ neobank trend, with companies like Coinbase, Crypto.com, and Binance launching banking features such as savings accounts, payment cards, and even lending services. The transition reflects a broader understanding that cryptocurrency adoption depends on practical utility in everyday transactions.

Why Major Crypto Companies Are Embracing Neobanking

Regulatory Compliance and Legitimacy

One of the primary drivers behind the crypto firms’ neobank trend is the pursuit of regulatory legitimacy. By obtaining banking licenses and adhering to financial regulations, crypto firms gain credibility with mainstream consumers and institutional investors. This regulatory compliance opens doors to partnerships with established financial institutions and reduces the stigma often associated with cryptocurrency platforms.

Neobank licenses require rigorous compliance standards, including Know Your Customer (KYC) protocols, Anti-Money Laundering (AML) measures, and consumer protection frameworks. While these requirements are demanding, they provide crypto companies with a competitive advantage in an increasingly regulated environment.

Revenue Diversification Strategy

The neobank trend offers crypto firms multiple revenue streams beyond trading fees. Banking services such as interest on deposits, interchange fees from debit cards, lending products, and subscription-based premium accounts create predictable, recurring revenue. This diversification is crucial during crypto market downturns when trading volumes plummet.

Traditional neobanks like Revolut and Chime have demonstrated that digital banking can be highly profitable. Crypto firms are following this blueprint while adding their unique advantage: native cryptocurrency integration. This hybrid model appeals to a broader customer base, from crypto enthusiasts to traditional banking customers curious about digital assets.

Customer Retention and Ecosystem Lock-in

By offering comprehensive financial services, crypto neobanks create powerful ecosystem effects that increase customer lifetime value. When users can handle all their financial needs—from paying bills to investing in Bitcoin—on a single platform, they’re less likely to switch to competitors. This stickiness is invaluable in the highly competitive fintech landscape.

The crypto firms’ neobank trend leverages network effects, where each additional service makes the platform more valuable. Users who initially sign up for crypto trading stay for the high-yield savings accounts, convenient payment cards, and seamless fiat-to-crypto conversions.

Key Features Driving the Crypto Neobank Trend

Seamless Fiat-to-Crypto Conversion

The hallmark of successful crypto neobanks is frictionless conversion between traditional currencies and digital assets. Users can instantly convert their salary deposits into cryptocurrency or vice versa without navigating multiple platforms or paying excessive fees. This convenience removes one of the biggest barriers to cryptocurrency adoption.

Crypto firms investing in the neobank trend prioritize instant settlement, competitive exchange rates, and transparent fee structures. These features make daily crypto usage practical rather than theoretical, encouraging mainstream adoption.

Multi-Currency Accounts and Global Accessibility

Modern crypto neobanks offer multi-currency accounts supporting dozens of fiat currencies alongside major cryptocurrencies. This global accessibility is particularly valuable for international freelancers, travelers, and businesses operating across borders. Traditional banks often charge hefty fees for currency conversion and international transfers—problems that crypto firms solve elegantly through blockchain technology.

The neobank trend in crypto emphasizes borderless finance, where geographic location doesn’t limit financial access. Users in emerging markets can access the same services as those in developed economies, promoting financial inclusion on an unprecedented scale.

Crypto-Backed Debit Cards

One of the most tangible manifestations of the crypto firms’ neobank trend is the proliferation of crypto-backed debit cards. These cards allow users to spend their cryptocurrency holdings at millions of merchants worldwide, automatically converting crypto to fiat at the point of sale. Some platforms even offer cashback rewards in cryptocurrency, creating additional incentives for everyday usage.

These cards bridge the gap between the digital asset world and traditional commerce, making cryptocurrency genuinely useful for daily expenses. The ability to seamlessly spend both fiat and crypto from the same account represents a major step toward mainstream crypto adoption.

Yield-Generating Savings Products

Crypto neobanks differentiate themselves from traditional banks by offering significantly higher interest rates on deposits. While conventional savings accounts might offer 0.5% annual interest, crypto firms frequently provide yields ranging from 4% to 10% or higher through various DeFi (Decentralized Finance) integrations and lending programs.

These high-yield products attract customers frustrated with negligible returns from traditional banks. However, the crypto firms’ neobank trend requires transparent communication about risks, as these yields often depend on cryptocurrency market conditions and aren’t always guaranteed or insured like traditional deposits.

Major Players Leading the Crypto Neobank Movement

Coinbase: From Exchange to Financial Hub

Coinbase, one of the world’s largest cryptocurrency exchanges, exemplifies the crypto firms’ neobank trend. The platform has expanded far beyond simple trading to offer Coinbase Card (a Visa debit card), direct deposit services, and even FDIC-insured USD accounts. By partnering with traditional banking infrastructure while maintaining its crypto-native features, Coinbase is building a comprehensive financial ecosystem.

The company’s strategic vision recognizes that becoming indispensable to users’ daily financial lives creates long-term competitive advantages. This approach reflects broader trends where crypto companies position themselves as complete financial solutions rather than specialized trading platforms.

Crypto.com: Banking Meets Blockchain

Crypto.com has aggressively pursued the neobank trend, offering metal prepaid cards with various reward tiers, crypto-earning opportunities, and a full-featured banking app. The platform’s strategy focuses on creating a lifestyle brand around cryptocurrency, making digital assets feel accessible and aspirational.

Their partnerships with traditional payment networks and focus on user experience demonstrate how crypto firms can successfully blend innovation with familiarity. Users get cutting-edge blockchain technology packaged in interfaces that feel as polished as traditional banking apps.

Binance: Global Scale Meets Local Banking

Binance’s approach to the crypto firms’ neobank trend leverages its massive global user base to launch localized banking services in multiple markets. Through Binance Card and various regional partnerships, the exchange is systematically building banking infrastructure that complements its dominant position in cryptocurrency trading.

The scale advantages enjoyed by major crypto firms like Binance allow them to negotiate favorable terms with payment processors, secure banking licenses in multiple jurisdictions, and invest heavily in compliance infrastructure—barriers that smaller competitors struggle to overcome.

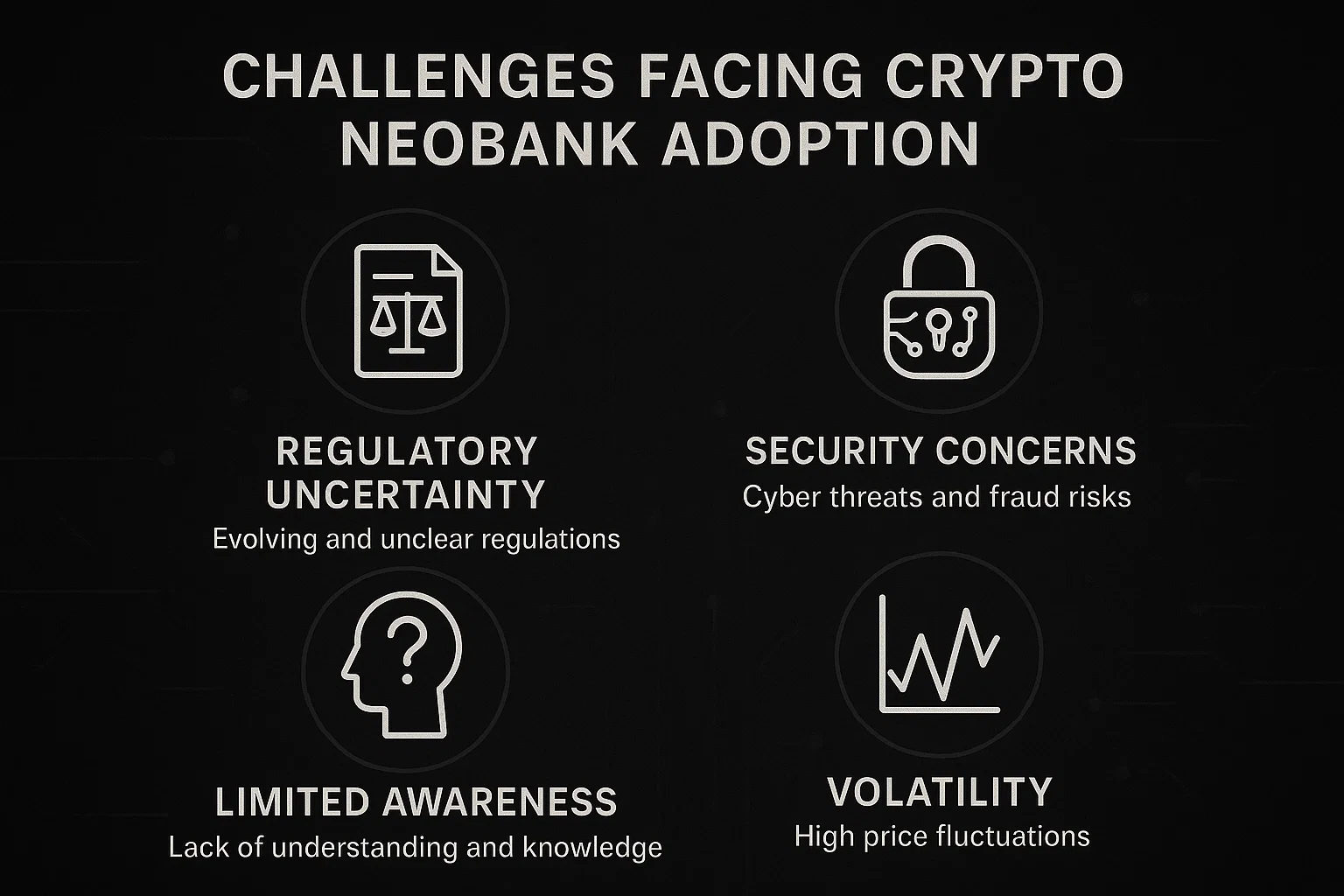

Challenges Facing Crypto Neobank Adoption

Regulatory Uncertainty and Compliance Costs

Despite the momentum behind the crypto firms’ neobank trend, regulatory challenges remain significant. Different jurisdictions have vastly different approaches to cryptocurrency regulation, forcing crypto companies to navigate a complex patchwork of requirements. Banking licenses are expensive and time-consuming to obtain, and maintaining compliance requires substantial ongoing investment.

The regulatory landscape continues evolving, with governments worldwide grappling with how to classify and regulate digital assets. This uncertainty creates risks for crypto neobanks that must adapt quickly to changing rules or face potential shutdowns and penalties.

Security and Consumer Protection Concerns

Security breaches and fraud remain existential threats to the neobank trend in crypto. Unlike traditional banks with extensive fraud protection and FDIC insurance, many crypto firms offer limited recourse when customers lose funds to hacks or scams. Building a robust security infrastructure while maintaining the convenience users expect requires constant vigilance and investment.

Consumer protection frameworks for crypto neobanks are still developing. Issues around custody, insurance, and liability in case of platform failures create uncertainty that may deter risk-averse customers from fully embracing these new financial services.

Technical Integration Complexity

Merging traditional banking infrastructure with blockchain technology presents significant technical challenges. Crypto firms must build systems that handle both legacy payment networks and cutting-edge blockchain protocols, ensuring seamless interoperability without compromising security or performance.

The crypto firms’ neobank trend requires substantial engineering talent and resources. Platforms must maintain uptime comparable to traditional banks (where even minutes of downtime are unacceptable) while managing the additional complexity of cryptocurrency networks with their own technical quirks and limitations.

Market Volatility and Financial Stability

Cryptocurrency’s infamous price volatility creates unique challenges for crypto neobanks offering traditional banking services. A sudden market crash can affect the platform’s liquidity, its ability to honor withdrawal requests, and customer confidence. Balancing crypto-native features with the stability expectations of traditional banking is a delicate act.

The neobank trend in crypto must address how these platforms will maintain operations during severe market downturns. Traditional banks have reserve requirements and regulatory oversight designed to ensure stability—frameworks that crypto firms are still adapting to their hybrid models.

The Future of Crypto Neobanking

Embedded Finance and API Integration

The next phase of the crypto firms’ neobank trend will likely involve embedded finance, where cryptocurrency and banking services are integrated directly into non-financial platforms. Through APIs, crypto neobanks can power financial features in e-commerce sites, gaming platforms, and social media apps, making digital assets ubiquitous across the internet.

This evolution transforms crypto firms from destination platforms into infrastructure providers, potentially reaching billions of users who may not even realize they’re using cryptocurrency-powered services. The embedded finance market is expected to exceed $7 trillion by 2030, offering enormous opportunities for innovative crypto companies.

Central Bank Digital Currencies (CBDCs) Integration

As governments worldwide develop Central Bank Digital Currencies (CBDCs), crypto neobanks are positioning themselves as potential distribution channels. These digital currencies issued by central banks could coexist with traditional cryptocurrencies, and crypto firms with established neobank infrastructure are well-positioned to integrate multiple forms of digital money.

The neobank trend may evolve to include seamless management of government-issued digital currencies, private cryptocurrencies, and traditional fiat—all within unified interfaces. This convergence could accelerate mainstream adoption and legitimize crypto firms as essential financial infrastructure.

DeFi Integration and Programmable Money

Decentralized Finance (DeFi) protocols offer financial services without traditional intermediaries, and crypto neobanks are beginning to integrate these capabilities. Future iterations of the crypto firms’ neobank trend may offer direct access to lending pools, automated yield optimization, and complex financial instruments previously available only to sophisticated investors.

This integration creates programmable money where users can set automated rules for savings, investments, and spending. The combination of user-friendly neobank interfaces with powerful DeFi capabilities could democratize access to sophisticated financial strategies, giving retail users tools previously reserved for institutions.

Cross-Industry Partnerships and Ecosystems

The maturation of the crypto firms’ neobank trend will likely accelerate partnerships between crypto companies and traditional financial institutions. Banks recognize they can’t ignore cryptocurrency demand, while crypto firms need banking infrastructure and regulatory expertise. These partnerships could create hybrid offerings combining each sector’s strengths.

Expect to see major banks offering cryptocurrency services through partnerships with crypto neobanks, and conversely, crypto firms leveraging traditional banking relationships to expand their service offerings. This convergence will blur the lines between traditional finance and crypto, making the neobank trend more mainstream.

Impact on Traditional Banking

Accelerating Digital Transformation

The crypto firms’ neobank trend is forcing traditional banks to accelerate their digital transformation efforts. As customers experience the speed, convenience, and innovation of crypto neobanks, they increasingly question why legacy banks can’t offer similar services. This competitive pressure is healthy for consumers, driving improvements across the financial sector.

Traditional banks are responding by launching their own digital-first offerings, partnering with fintech companies, and selectively adopting blockchain technology. The competition between crypto firms and established banks will likely result in better services, lower fees, and more innovation, benefiting all consumers.

Financial Inclusion Opportunities

Crypto neobanks are expanding financial access to underserved populations worldwide. By eliminating physical branch requirements and reducing minimum balance requirements, these platforms serve customers ignored by traditional banks. The global nature of cryptocurrency means someone in a developing country can access the same services as someone in a financial capital.

The neobank trend in crypto is particularly impactful in regions with unstable currencies or limited banking infrastructure. Crypto firms provide alternatives to unreliable local financial systems, offering dollarized accounts and global payment capabilities that were previously inaccessible to ordinary citizens.

Conclusion

The crypto firms’ neobank trend represents more than just a business strategy—it’s a fundamental reimagining of what financial services should look like in the digital age. By combining the innovation and efficiency of cryptocurrency with the practicality and familiarity of traditional banking, crypto firms are creating genuinely useful financial tools for everyday life.

As this trend accelerates, consumers gain access to financial services that are faster, cheaper, more transparent, and more globally accessible than ever before. While challenges around regulation, security, and stability remain, the momentum behind crypto neobanks appears unstoppable. The companies that successfully navigate this transition will likely define the future of finance for decades to come.

Read More: U.S. Charges Cambodian Tycoon Cryptocurrency Scam Case