The financial landscape is experiencing a fundamental transformation as blockchain technology payment services reshape how individuals and businesses conduct transactions globally. Within the first decade of blockchain’s existence, we’ve witnessed a paradigm shift from traditional banking systems to decentralised financial ecosystems that promise unprecedented security, transparency, and efficiency. As organisations worldwide recognise the limitations of legacy payment infrastructure, blockchain technology payment services emerge as the cornerstone of modern financial innovation, offering solutions that address long-standing challenges, including high transaction fees, slow settlement times, and geographical restrictions.

Blockchain Technology Payment Services

What Are Blockchain Technology Payment Services?

Blockchain technology payment services represent a revolutionary approach to processing financial transactions using distributed ledger technology. Unlike traditional payment systems that rely on centralised intermediaries such as banks and payment processors, blockchain payment solutions operate on decentralised networks where transactions are verified, recorded, and secured through cryptographic algorithms across multiple nodes.

These services leverage the fundamental characteristics of blockchain—immutability, transparency, and decentralisation—to create payment ecosystems that eliminate intermediaries, reduce costs, and accelerate transaction speeds. When a payment is initiated through blockchain technology payment services, it’s broadcast to a network of computers that validate the transaction through consensus mechanisms before permanently recording it on the blockchain.

The Core Components of Blockchain Payment Systems

Blockchain payment solutions consist of several interconnected components that work harmoniously to facilitate seamless transactions. The distributed ledger serves as the foundation, maintaining a chronological record of all transactions across the network. Smart contracts automate payment processes by executing predefined conditions without human intervention, while cryptocurrency wallets provide secure storage and management of digital assets.

Consensus mechanisms such as Proof of Work, Proof of Stake, or Delegated Proof of Stake ensure that all network participants agree on transaction validity before confirmation. These technical elements combine to create robust blockchain payment solutions that offer superior performance compared to conventional systems.

How Blockchain Technology Payment Services Transform Transactions

Enhanced Security and Fraud Prevention

Security stands as the paramount advantage of blockchain technology payment services. Traditional payment systems remain vulnerable to various cyber threats, including data breaches, identity theft, and fraudulent transactions. Blockchain’s cryptographic security creates an almost impenetrable fortress around financial data.

Each transaction undergoes encryption and links to the previous transaction through complex mathematical algorithms, forming an immutable chain that cannot be altered retroactively. This architecture makes it extraordinarily difficult for malicious actors to manipulate transaction records or steal sensitive information. The decentralised nature of blockchain payment platforms means there’s no single point of failure that hackers can target, distributing risk across the entire network.

Transparency and Traceability

Transparency represents another transformative aspect of blockchain payment solutions. Every transaction recorded on the blockchain becomes visible to all network participants, creating an audit trail that enhances accountability. While maintaining user privacy through pseudonymous addresses, the system allows stakeholders to verify transactions independently without relying on third-party auditors.

This transparency proves particularly valuable for businesses requiring rigorous compliance with regulatory standards. Companies can demonstrate transaction legitimacy, track fund movements, and ensure adherence to anti-money laundering regulations through blockchain’s inherent traceability features.

Reduced Transaction Costs

Traditional payment systems impose substantial fees through multiple intermediaries involved in processing transactions. Banks, payment processors, and clearing houses each extract their share, significantly increasing the overall cost of transactions, especially for cross-border payments. Blockchain technology payment services dramatically reduce these expenses by eliminating intermediaries.

By facilitating peer-to-peer transactions, blockchain payment systems bypass traditional financial institutions, allowing users to transfer value directly. This disintermediation results in cost savings ranging from 40% to 80% compared to conventional payment methods, making blockchain payment processing particularly attractive for international remittances and business-to-business transactions.

Accelerated Settlement Times

Speed constitutes a critical factor in modern payment ecosystems. Traditional cross-border transactions often require three to five business days for settlement due to multiple intermediary banks and clearing processes. Blockchain technology payment services revolutionise this aspect by enabling near-instantaneous settlements.

Transactions on blockchain networks typically confirm within minutes or even seconds, depending on the specific protocol and network congestion. This acceleration eliminates the frustration of delayed payments and improves cash flow management for businesses. The 24/7 operational capability of blockchain networks ensures the transaction process continues continuously without being restricted by banking hours or holidays.

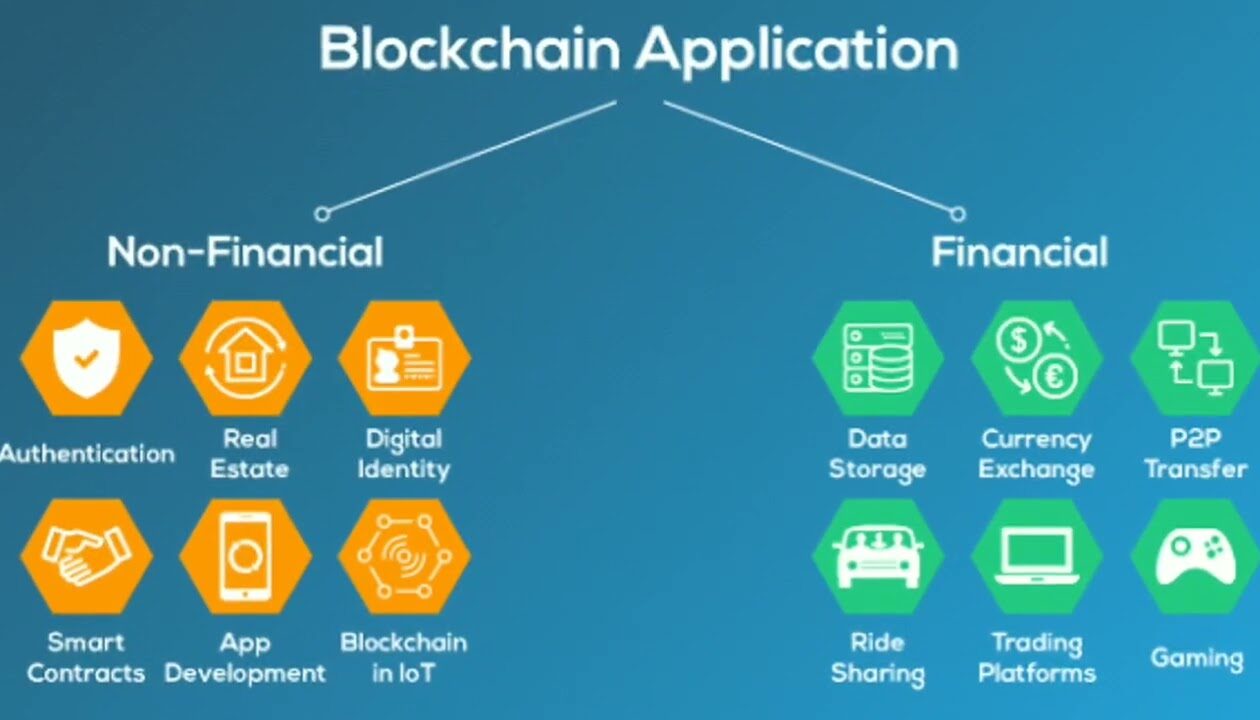

Real-World Applications of Blockchain Technology Payment Services

Cross-Border Remittances

The global remittance market, valued at over $700 billion annually, suffers from high fees and slow processing times. Blockchain technology payment services address these challenges by providing efficient alternatives to traditional money transfer operators. Companies leveraging blockchain for remittances enable migrant workers to send money home with minimal fees and near-instant delivery.

These blockchain payment solutions prove especially beneficial for unbanked populations in developing countries, providing financial inclusion opportunities previously unavailable through conventional banking systems. Recipients can access funds through mobile wallets or cryptocurrency exchanges, bypassing the need for traditional bank accounts.

E-Commerce and Retail Payments

Online merchants increasingly adopt blockchain technology payment services to enhance customer experience and reduce operational costs. Cryptocurrency payment processors integrate seamlessly with e-commerce platforms, allowing businesses to accept Bitcoin, Ethereum, and other digital currencies alongside traditional payment methods.

These digital payment innovation solutions eliminate chargeback fraud, a persistent problem costing merchants billions annually. Once confirmed on the blockchain, transactions become irreversible, protecting businesses from fraudulent refund requests while maintaining consumer protection through alternative dispute resolution mechanisms.

Supply Chain Finance

Supply chain management benefits tremendously from blockchain financial services by enabling transparent tracking of goods and automated payment releases. Smart contracts trigger payments automatically when shipment milestones are achieved, eliminating delays associated with manual verification processes.

This automation streamlines working capital management, allowing suppliers to receive payments faster while giving buyers greater visibility into their supply chain operations. The immutable record of transactions also simplifies auditing and compliance procedures across complex global supply chains.

Healthcare Payment Processing

The healthcare industry grapples with administrative inefficiencies costing billions annually. Blockchain technology payment services offer solutions by automating insurance claim processing, reducing administrative overhead, and preventing billing fraud. Smart contracts can automatically verify patient eligibility, process claims, and settle payments between healthcare providers and insurers.

This blockchain payment processing approach accelerates reimbursement cycles, allowing medical facilities to improve cash flow while reducing the administrative burden on healthcare professionals. Patients benefit from transparent billing and streamlined payment experiences.

Advantages of Implementing Blockchain Technology Payment Services

Financial Inclusion

Blockchain payment solutions democratize access to financial services by removing barriers imposed by traditional banking systems. Approximately 1.7 billion adults globally remain unbanked, lacking access to basic financial services. Blockchain technology requires only internet connectivity and a smartphone, enabling these populations to participate in the global economy.

Decentralised payment platforms provide banking alternatives for individuals in regions with underdeveloped financial infrastructure, empowering them with tools to save, invest, and transact digitally. This financial inclusion drives economic development and reduces poverty in underserved communities.

Programmable Money

Smart contracts transform money into programmable assets through blockchain technology payment services. These self-executing agreements enable conditional payments that automatically release funds when predetermined criteria are met. This capability creates opportunities for innovative financial products and services.

Subscription services can automate recurring payments, freelance platforms can implement milestone-based compensation, and escrow services can hold funds until contractual obligations are fulfilled. The programmability of blockchain payments eliminates manual intervention, reducing errors and disputes.

Data Sovereignty

Traditional payment systems require users to surrender control of personal financial data to centralised institutions. Blockchain payment platforms return data sovereignty to individuals, allowing them to maintain ownership and control of their financial information. Users decide what information to share and with whom, enhancing privacy protections.

This paradigm shift aligns with growing concerns about data privacy and gives individuals greater agency over their digital identities. Blockchain’s cryptographic techniques ensure that sensitive information remains secure while enabling necessary verification processes.

Interoperability

Modern blockchain technology payment services increasingly focus on interoperability, allowing different blockchain networks to communicate and exchange value seamlessly. Cross-chain protocols and atomic swaps enable users to transact across multiple blockchain ecosystems without converting currencies through centralised exchanges.

This interoperability creates a more connected financial ecosystem where value flows freely between networks, enhancing liquidity and user choice. Businesses can accept payments in various cryptocurrencies while maintaining operational simplicity through unified interfaces.

Challenges Facing Blockchain Technology Payment Services

Regulatory Uncertainty

Despite their promise, blockchain payment solutions navigate complex regulatory landscapes that vary significantly across jurisdictions. Governments worldwide grapple with how to classify, regulate, and tax cryptocurrency transactions, creating uncertainty for businesses and consumers.

Regulatory clarity remains essential for mainstream adoption of blockchain technology payment services. Forward-thinking jurisdictions that establish clear frameworks attract innovation while protecting consumers, positioning themselves as blockchain payment hubs. However, regulatory fragmentation across borders complicates international transactions and compliance efforts.

Scalability Limitations

Many blockchain networks face scalability challenges when processing high transaction volumes. Bitcoin and Ethereum have experienced network congestion during peak usage periods, resulting in slower confirmation times and increased transaction fees. These limitations hinder the ability of blockchain payment systems to compete with traditional payment processors that handle thousands of transactions per second.

Layer-2 solutions, sharding technologies, and alternative consensus mechanisms aim to address these scalability concerns. As these innovations mature, blockchain technology payment services will achieve the throughput necessary for global adoption.

User Experience Barriers

Cryptocurrency wallets, private keys, and blockchain interfaces can intimidate non-technical users. The irreversible nature of blockchain transactions means mistakes can result in permanent loss of funds, creating anxiety for new users. Improving user experience represents a critical challenge for blockchain payment solutions.

Wallet providers and payment platforms increasingly focus on simplifying interfaces, implementing recovery mechanisms, and providing educational resources. As user experience improves, blockchain technology payment services will become accessible to mainstream audiences.

Volatility Concerns

Cryptocurrency price volatility presents challenges for blockchain payment processing. Merchants accepting cryptocurrency payments risk value fluctuations between transaction time and conversion to fiat currency. While stablecoins—cryptocurrencies pegged to stable assets like the US dollar—address this concern, adoption remains gradual.

Payment processors increasingly offer instant conversion services that lock in fiat equivalent values at transaction time, protecting merchants from volatility while maintaining the benefits of blockchain technology payment services.

The Future of Blockchain Technology Payment Services

Central Bank Digital Currencies (CBDCs)

Central banks worldwide explore blockchain technology to issue digital currencies that combine the benefits of cryptocurrency with the stability of government-backed fiat money. CBDCs represent a convergence of traditional finance and blockchain payment solutions, potentially transforming how monetary policy is implemented and how citizens interact with national currencies.

These digital currencies could enhance financial inclusion, reduce payment system costs, and provide governments with improved tools for economic management. As CBDCs launch globally, they will accelerate the adoption of blockchain technology payment services across all sectors.

Integration with Emerging Technologies

The convergence of blockchain with artificial intelligence, Internet of Things, and 5G connectivity will unlock new possibilities for blockchain payment platforms. IoT devices equipped with cryptocurrency wallets could autonomously initiate and process payments, enabling machine-to-machine transactions.

AI algorithms could optimise payment routing across blockchain networks, selecting the most efficient and cost-effective paths for transactions. These technological synergies will expand the capabilities and applications of blockchain technology payment services beyond current imagination.

Institutional Adoption

Major financial institutions increasingly recognise the potential of blockchain financial services. Banks experiment with blockchain for settlement systems, payment rails, and customer services. Payment giants like Visa and Mastercard integrate cryptocurrency capabilities into their networks, legitimising digital assets and expanding merchant acceptance.

This institutional adoption validates blockchain technology payment services and accelerates mainstream integration. As traditional finance embraces blockchain, hybrid systems will emerge that combine the reliability of established institutions with the innovation of decentralised networks.

Enhanced Privacy Features

Privacy-focused blockchain protocols develop advanced cryptographic techniques that enable confidential transactions while maintaining regulatory compliance. Zero-knowledge proofs allow transaction verification without revealing sensitive information, addressing privacy concerns while satisfying audit requirements.

These privacy enhancements will make blockchain payment solutions suitable for industries with strict confidentiality requirements, including healthcare, legal services, and corporate finance. Balancing transparency with privacy represents the next evolution of blockchain technology payment services.

Implementing Blockchain Technology Payment Services: Best Practices

Choosing the Right Blockchain Platform

Organisations considering blockchain payment solutions must evaluate various blockchain platforms based on their specific requirements. Factors to consider include transaction speed, security features, scalability, development ecosystem, and regulatory compliance capabilities.

Ethereum remains popular for smart contract functionality, while Bitcoin offers unparalleled security and network effects. Newer platforms like Solana and Avalanche provide high throughput for applications requiring rapid transaction processing. Enterprise-focused blockchains like Hyperledger offer permissioned networks with enhanced privacy controls suitable for corporate applications.

Security Implementation

Security must be paramount when deploying blockchain technology payment services. Organisations should implement multi-signature wallets requiring multiple approvals for significant transactions, establish robust key management procedures, and conduct regular security audits.

Cold storage solutions protect large cryptocurrency holdings from online threats, while hot wallets facilitate daily operational needs. Employee training on security best practices prevents social engineering attacks and ensures the responsible handling of digital assets.

Compliance and Regulatory Adherence

Successful implementation of blockchain payment platforms requires careful attention to regulatory requirements. Organisations should establish know-your-customer (KYC) and anti-money laundering (AML) procedures compliant with applicable jurisdictions.

Engaging legal counsel familiar with cryptocurrency regulations helps navigate the complex regulatory landscape. Proactive compliance demonstrates commitment to operating within legal frameworks, building trust with regulators, customers, and partners.

Customer Education

Educating customers about blockchain technology payment services facilitates adoption and reduces support inquiries. Providing clear documentation, tutorial videos, and responsive customer support helps users navigate new payment methods confidently.

Transparency about transaction processes, fee structures, and security measures builds trust and encourages usage. As customers become comfortable with blockchain payments, they increasingly appreciate the benefits and advocate for wider adoption.

Conclusion

Blockchain technology payment services represent more than technological innovation—they embody a fundamental reimagining of how value transfers occur in the digital age. By eliminating intermediaries, reducing costs, accelerating settlements, and enhancing security, blockchain payments address critical limitations of traditional financial systems.

While challenges, including regulatory uncertainty, scalability constraints, and user experience barriers, remain, ongoing innovation continues to resolve these obstacles. The trajectory is clear: blockchain payment solutions will increasingly dominate the financial landscape as technology matures and adoption accelerates.