The financial landscape is experiencing a seismic shift, and at the heart of this transformation lies blockchain technology for payment services. Traditional payment systems, plagued by inefficiencies, high transaction costs, and security vulnerabilities, are being challenged by a revolutionary approach that promises transparency, speed, and unprecedented security. As businesses and consumers worldwide seek faster, more reliable ways to transfer value, blockchain emerges not just as an alternative but as a fundamental reimagining of how payments should work in the digital age. This technology, originally designed to support cryptocurrencies, has evolved into a comprehensive solution that addresses the most pressing challenges facing modern payment infrastructure.

Financial institutions, fintech startups, and enterprise organizations are increasingly recognizing that blockchain technology for payment services represents more than just incremental improvement—it’s a paradigm shift that eliminates intermediaries, reduces settlement times from days to seconds, and provides an immutable record of every transaction. Whether you’re a business owner looking to optimize payment processing, a developer exploring decentralized finance, or simply curious about the future of money, understanding how blockchain is reshaping payment services is essential for navigating tomorrow’s financial ecosystem.

Blockchain Technology in Payment Systems

At its core, blockchain technology for payment services operates as a distributed ledger system that records transactions across multiple computers simultaneously. Unlike traditional centralized databases controlled by single entities, blockchain creates a network where every participant maintains an identical copy of the transaction history. This fundamental architecture eliminates single points of failure and creates an environment where trust is mathematically guaranteed rather than dependent on institutional reputation.

The technology employs cryptographic principles to secure each transaction, linking blocks of data together in an immutable chain. When someone initiates a payment, the transaction gets broadcast to the network, validated by multiple nodes through consensus mechanisms, and permanently recorded in a block that becomes part of the chain. This process ensures that once a transaction is confirmed, it cannot be altered or reversed without consensus from the network, providing unparalleled security and transparency.

How Blockchain Transforms Traditional Payment Processing

Traditional payment systems typically involve multiple intermediaries—banks, payment processors, clearinghouses, and card networks—each adding layers of complexity, time, and cost to transactions. A simple credit card payment might touch five or more institutions before completion, with settlement taking days and fees accumulating at each step.

Blockchain technology for payment services eliminates these intermediaries by enabling peer-to-peer transactions that are verified and recorded by the network itself. Smart contracts can automate payment conditions, executing transfers instantly when predetermined criteria are met. This disintermediation dramatically reduces transaction costs, accelerates settlement times, and provides real-time visibility into payment status—benefits that resonate strongly with businesses operating in global markets.

The transparency inherent in blockchain systems also addresses a critical pain point in traditional payments: reconciliation. Organizations spend countless hours matching payment records across different systems, resolving discrepancies, and tracking transaction histories. With blockchain, all parties view the same immutable ledger, making reconciliation instantaneous and disputes far easier to resolve.

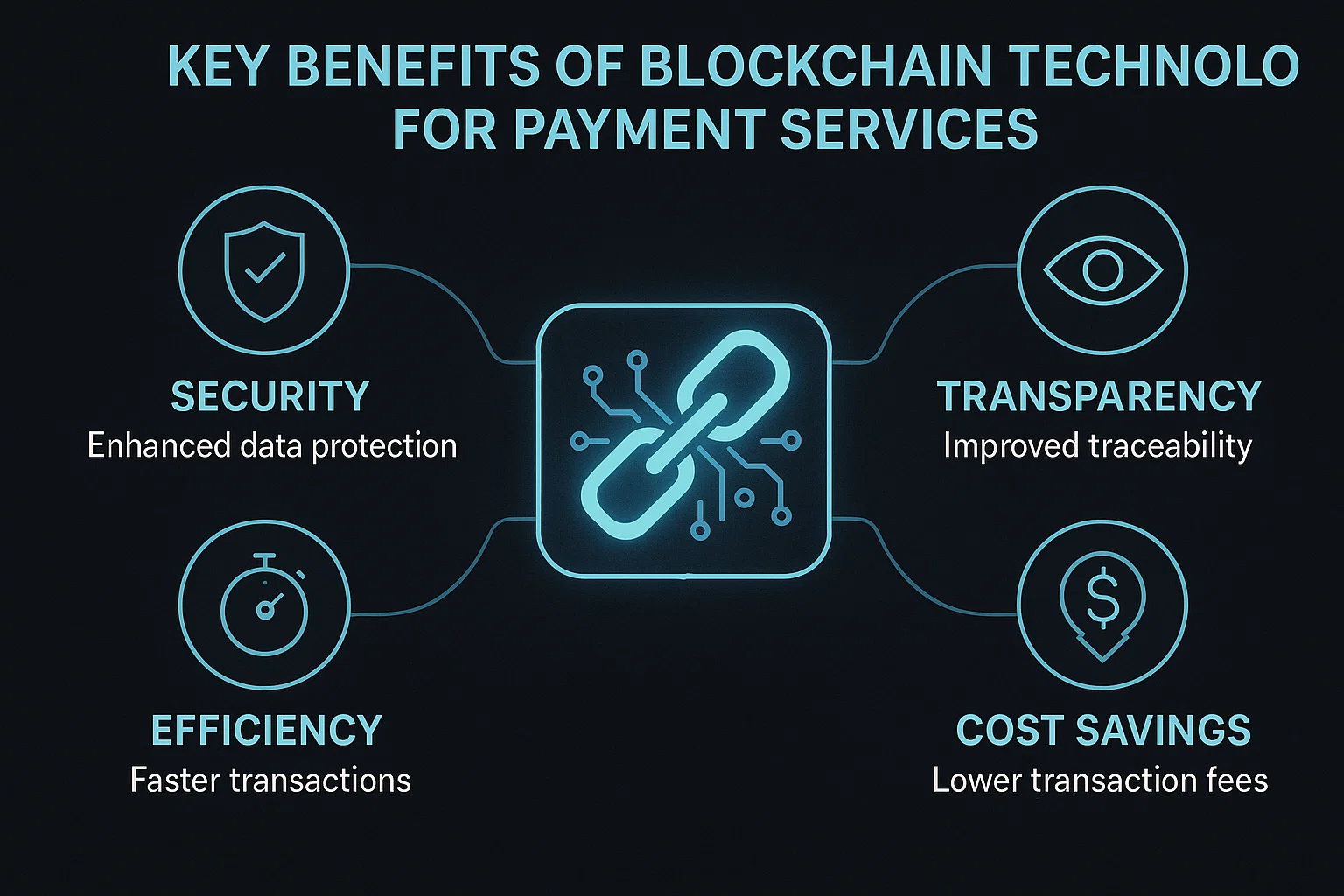

Key Benefits of Blockchain Technology for Payment Services

The advantages of implementing blockchain technology for payment services extend far beyond simple cost savings. Organizations adopting this technology report transformative improvements across multiple dimensions of their payment operations, fundamentally changing how they interact with customers, partners, and financial systems.

Enhanced Security and Fraud Prevention

Security represents perhaps the most compelling benefit of blockchain-based payment systems. Traditional payment infrastructure suffers from vulnerability to various attack vectors—data breaches, identity theft, payment fraud, and system compromises regularly make headlines. The centralized nature of conventional systems creates attractive targets for cybercriminals who can potentially access vast amounts of sensitive financial data through a single breach.

Blockchain’s decentralized architecture fundamentally changes this security paradigm. Rather than storing sensitive payment information in centralized databases, blockchain distributes encrypted transaction data across thousands of nodes. Altering transaction history would require simultaneously compromising more than half the network—a feat that becomes exponentially more difficult and expensive as networks grow. Cryptographic signatures ensure that only authorized parties can initiate transactions, while the transparency of the ledger makes fraudulent activity immediately visible to network participants.

This security model has proven particularly valuable for cross-border payments, where fraud rates in traditional systems can reach significant percentages. Organizations implementing blockchain technology for payment services report dramatic reductions in chargebacks, identity fraud, and unauthorized transaction attempts.

Dramatically Reduced Transaction Costs

Payment processing fees constitute a substantial expense for businesses, particularly those operating internationally or processing high volumes of small transactions. Traditional payment systems impose multiple fee layers—interchange fees, assessment fees, processing fees, and cross-border charges—that collectively can consume three to five percent of transaction values. For businesses with thin margins, these costs significantly impact profitability.

Blockchain technology for payment services removes many intermediaries that extract fees from the payment chain. By enabling direct peer-to-peer transfers, blockchain reduces processing costs to fractions of a percent. International transfers, which traditionally incur substantial fees and currency conversion charges, become dramatically cheaper when conducted through blockchain networks that support multiple currencies or utilize stablecoins pegged to fiat values.

Small businesses and e-commerce operations particularly benefit from these cost reductions. Merchants accepting credit cards typically pay two to three percent per transaction plus fixed fees—costs that blockchain payments can reduce by seventy-five percent or more. These savings can be passed to customers, reinvested in business growth, or used to improve bottom-line profitability.

Accelerated Settlement and Real-Time Payments

Traditional payment settlement operates on antiquated infrastructure, with bank transfers taking multiple business days and international payments requiring even longer. This settlement lag creates cash flow challenges for businesses, ties up working capital, and introduces risk during the settlement period. The delay stems from batch processing systems, banking hours limitations, and the complex web of correspondent banking relationships required for international transfers.

Implementing blockchain technology for payment services transforms settlement from a multi-day process to a real-time operation. Transactions are validated and recorded within minutes or even seconds, depending on the blockchain protocol used. For businesses, this means immediate access to funds, improved cash flow management, and the ability to operate with reduced working capital reserves.

The impact extends beyond pure speed. Real-time settlement eliminates the concept of payment float—the period during which funds are in transit but accessible to neither party. This clarity benefits both payers and payees, reducing disputes about payment timing and enabling more precise financial planning. Supply chain operations particularly benefit from instant settlement, as payments can be automatically triggered upon delivery confirmation, creating seamless just-in-time payment systems.

Applications of Blockchain Technology for Payment Services

The versatility of blockchain technology for payment services manifests across diverse use cases, each addressing specific pain points in traditional payment infrastructure. Organizations across industries are discovering innovative applications that leverage blockchain’s unique characteristics to solve longstanding challenges.

Cross-Border and International Payments

International money transfers represent one of the most compelling applications for blockchain-based payment systems. Traditional cross-border payments involve multiple correspondent banks, currency conversions through forex markets, compliance checks across different regulatory regimes, and settlement through systems like SWIFT that were designed decades ago. This complexity results in transactions taking three to five business days, costing fifteen to thirty dollars on average, and suffering from limited transparency during transit.

Blockchain technology for payment services addresses each of these limitations simultaneously. Blockchain networks operate globally without regard for national borders, enabling direct transfers between parties in different countries without correspondent banking chains. Transactions settle in minutes rather than days, with full transparency allowing both parties to track payment status in real-time. Costs drop dramatically, often to single-digit dollars or less, even for large transfers.

Remittance markets, where workers send money to family members in other countries, particularly benefit from blockchain solutions. Traditional remittance services charge average fees exceeding six percent of transfer amounts—a significant burden for individuals sending modest sums. Blockchain-based remittance platforms reduce these fees to one to two percent while accelerating delivery from days to hours.

Business-to-Business Payment Solutions

Commercial payments between businesses suffer from many inefficiencies that blockchain effectively addresses. Invoice processing, payment reconciliation, and managing payment terms across multiple vendors consume substantial administrative resources. Payment disputes, delayed settlements, and tracking payment status across different banking systems create friction in business relationships.

Organizations implementing blockchain technology for payment services for B2B transactions benefit from smart contract automation that can encode payment terms directly into the blockchain. Invoices can be automatically verified against delivery confirmations, triggering payments when conditions are satisfied without manual intervention. This automation reduces processing costs, eliminates payment delays caused by manual approval workflows, and provides both parties with transparent, real-time visibility into payment status.

Supply chain finance applications demonstrate particular promise. Suppliers often face cash flow challenges when customers demand extended payment terms. Blockchain enables innovative financing arrangements where verified invoices become instantly tradable assets, allowing suppliers to receive payment immediately while financiers acquire the receivable at a discount—all recorded transparently on the blockchain.

Micropayments and Content Monetization

Traditional payment systems economically prohibit very small transactions due to fixed and percentage-based fees. Charging consumers fifty cents for digital content becomes impractical when payment processing costs thirty cents. This limitation has constrained business models for digital content, forcing creators toward advertising-supported or subscription models even when pay-per-use would better serve consumer preferences.

Blockchain technology for payment services enables economically viable micropayments by reducing transaction costs to negligible amounts. Content creators can charge pennies or fractions of pennies for articles, videos, songs, or other digital goods without payment processing eroding revenue. Blockchain-based micropayment systems have enabled new business models in media, gaming, and digital services where consumption-based pricing becomes practical for the first time.

This capability extends beyond content to machine-to-machine payments in Internet of Things ecosystems. Devices can automatically pay for resources consumed—computing power, data storage, bandwidth, or electricity—with tiny payments settling instantly via blockchain. These micropayment capabilities enable entirely new economic models for the sharing economy and distributed computing resources.

Implementing Blockchain Payment Solutions: Considerations and Challenges

While blockchain technology for payment services offers compelling benefits, successful implementation requires careful consideration of technical, regulatory, and operational factors. Organizations must navigate various challenges to realize blockchain’s full potential in their payment operations.

Scalability and Performance Requirements

Early blockchain networks faced significant scalability limitations, with Bitcoin processing roughly seven transactions per second and Ethereum handling fiftee, —far below the thousands of transactions per second required for mainstream payment applications. These constraints stem from the decentralization and security features central to blockchain design, creating inherent trade-offs between decentralization, security, and scalability.

Modern blockchain platforms designed specifically for blockchain technology for payment services have addressed these limitations through various innovations. Layer-2 solutions process transactions off the main blockchain, settling final balances periodically while maintaining security guarantees. Newer consensus mechanisms like proof-of-stake dramatically increase transaction throughput while reducing energy consumption. Enterprise blockchain platforms like Hyperledger Fabric offer permissioned networks optimized for high-volume business transactions.

Organizations evaluating blockchain payment solutions must assess their scalability requirements and select platforms capable of handling peak transaction volumes with acceptable latency. Hybrid approaches combining public blockchain security with private network performance often provide optimal solutions for enterprise payment needs.

Regulatory Compliance and Legal Frameworks

The regulatory landscape surrounding blockchain technology for payment services continues evolving as governments worldwide develop frameworks for digital assets and decentralized payment systems. Organizations must navigate complex requirements across multiple jurisdictions, particularly for cross-border payment applications.

Anti-money laundering regulations, know-your-customer requirements, and counter-terrorism financing rules apply to blockchain payment systems just as they do to traditional payments. Implementing compliant solutions requires integrating identity verification, transaction monitoring, and reporting capabilities while preserving blockchain’s efficiency benefits. Privacy-focused blockchains face particular scrutiny from regulators concerned about transparency for law enforcement purposes.

Leading blockchain payment platforms have developed compliance frameworks that satisfy regulatory requirements while leveraging blockchain advantages. These solutions incorporate identity verification at network entry points, maintain audit trails for regulatory reporting, and implement transaction screening against sanctions lists—demonstrating that blockchain technology for payment services can meet the highest compliance standards.

Integration with Existing Payment Infrastructure

Most organizations cannot immediately replace their entire payment infrastructure with blockchain-based systems. Practical adoption of blockchain technology for payment services requires integration with existing banking systems, accounting platforms, enterprise resource planning software, and legacy payment processors. This integration challenge often determines adoption timelines and success.

Successful implementations typically employ hybrid approaches where blockchain handles specific payment functions while interfacing with traditional systems at integration points. Payment gateways that accept blockchain transactions and settle in fiat currency provide bridges between blockchain and traditional finance. APIs and middleware platforms enable blockchain payment data to flow into existing financial management systems without requiring wholesale software replacements.

Organizations should prioritize use cases where blockchain delivers maximum value with minimum integration complexity. Isolated payment flows like international transfers, specific vendor payments, or new digital products may provide initial entry points that prove blockchain’s value before expanding to core payment operations.

The Future of Blockchain Technology for Payment Services

The trajectory of blockchain technology for payment services points toward increasing adoption across financial services and progressive integration into mainstream payment infrastructure. Several trends suggest how this technology will continue evolving and reshaping payment systems.

Central Bank Digital Currencies and Stablecoins

Central banks worldwide are exploring or actively developing digital currencies built on blockchain infrastructure. These central bank digital currencies represent government-backed digital payment instruments that combine blockchain technology’s efficiency with the stability and trust of national currencies. Countries including China, Sweden, and the Bahamas have already launched or piloted CBDCs, with many others in development phases.

Stablecoins—cryptocurrencies pegged to fiat currency values—provide another bridge between blockchain technology for payment services and traditional finance. These instruments offer blockchain’s speed and efficiency while minimizing cryptocurrency volatility concerns. Major financial institutions and technology companies have launched stablecoin initiatives, recognizing their potential to serve as digital payment rails for blockchain-based transactions.

The convergence of CBDCs, stablecoins, and blockchain payment infrastructure suggests a future where digital currency becomes the native format for blockchain payments, eliminating currency exchange friction and further accelerating adoption.

Interoperability and Cross-Chain Payment Networks

Current blockchain ecosystems often operate in isolation, with limited ability to transfer value between different blockchain networks. This fragmentation constrains blockchain technology for payment services by requiring parties to adopt the same blockchain platform. The future points toward interoperability solutions that enable seamless cross-chain transactions, allowing payments to flow between different blockchain networks as easily as between bank accounts.

Cross-chain bridges, atomic swaps, and interoperability protocols are emerging to connect disparate blockchain networks. These technologies will enable truly universal blockchain payment systems where the specific blockchain platform becomes invisible to users, similar to how email users can communicate across different email providers without considering underlying technical differences.

This interoperability will accelerate blockchain payment adoption by eliminating network effects that currently favor established platforms. Businesses will choose blockchain solutions based on specific features rather than worrying about which networks their customers and partners use.

Artificial Intelligence and Blockchain Payment Optimization

The integration of artificial intelligence with blockchain technology for payment services promises sophisticated optimization of payment operations. AI algorithms can analyze blockchain payment patterns to optimize transaction timing, predict network congestion, and dynamically route payments through the most efficient channels. Machine learning models can enhance fraud detection by identifying suspicious transaction patterns across the transparent blockchain ledger.

Smart contracts incorporating AI decision-making could enable adaptive payment systems that automatically adjust payment terms based on market conditions, counterparty behavior, or business performance metrics. This convergence of AI and blockchain will create increasingly autonomous payment systems requiring minimal human intervention while maintaining transparency and security.

Choosing the Right Blockchain Payment Solution

Organizations ready to implement blockchain technology for payment services face numerous platform and solution choices. Selecting the right approach requires evaluating several critical factors aligned with business requirements and strategic objectives.

Evaluating Blockchain Platforms and Networks

Different blockchain platforms offer varying characteristics suited to different payment use cases. Public blockchains like Bitcoin and Ethereum provide maximum decentralization and securi,ty but may have scalability limitations. Enterprise blockchains like Hyperledger and Corda offer higher performance with permissioned access suitable for business networks. Newer platforms like Solana and Avalanche claim high throughput while maintaining decentralization.

Organizations should evaluate platforms based on transaction speed, cost per transaction, finality time, security model, developer ecosystem, and regulatory positioning. The choice between public and private blockchains depends on whether transparency to external parties provides value or represents a competitive concern. Hybrid solutions combining public blockchain security with private network performance often provian de optimal balance for blockchain technology for payment services.

Assessing Vendor Solutions and Implementation Partners

Many organizations choose to work with specialized vendors providing turnkey blockchain payment solutions rather than developing custom implementations. Evaluating vendors requires examining their track record, regulatory compliance capabilities, integration flexibility, and long-term viability. The blockchain space includes both established financial technology companies and innovative startups—each offering different advantages.

Implementation partners with expertise in both blockchain technology and payment systems prove invaluable for successful deployments. These partners can navigate technical complexity, regulatory requirements, and change management challenges that organizations face when adopting blockchain technology for payment services. Reference checking with organizations that have completed similar implementations provides crucial insights into vendor capabilities and potential pitfalls.

Conclusion

The evidence is clear: blockchain technology for payment services is not a distant future possibility but a present-day reality transforming how value transfers across borders, industries, and business models. Organizations that embrace this technology gain competitive advantages through reduced costs, faster settlements, enhanced security, and capabilities impossible with traditional payment infrastructure.

Success requires more than simply adopting new technology—it demands reimagining payment processes, challenging assumptions about how transactions must work, and committing to the organizational change necessary for transformation. Whether you begin with a pilot project addressing a specific pain point or pursue comprehensive blockchain payment integration, the journey starts with understanding the technology’s potential and taking concrete steps toward implementation.

Read More: Blockchain Technology Revolutionising Decentralised Systems